The most difficult and annoying part of decentralized finance (defi) today is undoubtedly its user experience — fragmented, slow, risky, and frankly, broken. Wrapping defi within beautiful, easy-to-use centralized finance (cefi) frontends is becoming an increasingly popular strategy for both new and existing market players. In these types of setups, the user (happily) pays a small premium for great UX, while the company benefits from that premium.

This pattern isn’t necessarily new — we’re beginning to see small examples of defi “modules” that live directly within cefi platforms. The most basic example is Coinbase passing staking yield onto consumers (after taking a 35% cut). But recently, companies have been exploring more creative ways to package defi and upsell it.

For example, Coinbase just announced Bitcoin-backed loans up to $100k in USDC (powered by Morpho) directly within their own UI. Borrowing USDC against Bitcoin is not a new concept — it has been readily available for years on defi platforms like Aave and Compound. This route, though, annoyingly requires users to deposit from a centralized exchange, wrap their Bitcoin for wBTC, and finally, take out a loan. The differentiation in Coinbase’s solution lies in their existing distribution combined with a UI where users don’t have to leave the web app to get a Bitcoin-backed loan. And for Coinbase, it’s a win-win:

The loans drive volume and demand for USDC on Base (Coinbase’s L2, where Morpho operates).

Coinbase can then take their notoriously high fees on whatever the user does with the USDC on their frontend.

In Q3 2024, Coinbase made ~$34mm from Base and ~$500mm from their centralized exchange; clearly, their incentives are to drive volume towards their frontends. If they can do this while also funneling activity towards Base — like in case of loans — it’s the best of both worlds.

Many years ago, Coinbase actually did experiment with allowing users to get defi yield on their holdings, powered by Compound on the backend (Coinbase Ventures’ first investment). There was also a brief period where users could lend out ETH and other assets, as opposed to just USDC. These features operated in a regulatory grey area and Coinbase eventually discontinued them, but as is the case with any rapidly growing industry: what’s old is eventually new again.

It’s also worth noting that there are brand-new, noncustodial solutions in the market like Lava, which allows customers to take out a USDC loan (on Solana) of any size against their BTC directly in their mobile app, and then are able to spend the USDC with a Visa card. Companies like these are still “packaging” defi into a nice, seamless UX, but are generally more custom-built for one specific purpose versus attempting to be an all-in-one financial platform.

Following Coinbase’s playbook, Robinhood is also leveraging their distribution to introduce more cryptonative products to their users. Their CEO wants to tokenize private markets to democratize participation, they are rolling out BTC futures (just as Coinbase filed for Solana futures with the CFTC), and their Robinhood Wallet mobile app (for crypto trading) has been steadily gaining traction.

Within the month of January alone, Robinhood increased their tradeable crypto assets (on their main app) from 15 to 22, showing they’re moving at a much more rapid pace on the listings side (and are also newly emboldened by a Trump presidency). Robinhood’s crypto trading fees are also roughly half of Coinbase’s — which helps them compete — although their selection is relatively limited on their non-Wallet app (only 22 crypto assets listed at the time of writing this compared to Coinbase’s 300+).

Despite lower fees, Robinhood’s business is ripping: their revenue doubled last quarter, their crypto revenue increased ~700% to $358 million, and they had $50 billion in net deposits in 2024. On the latest earnings call, their founder Vlad Tenev mentioned:

They’re exploring staking as the regulatory guidance and clarity improves.

They want to tokenize private company shares as well as public securities.

They’re using stablecoins to power a lot of their weekend settlements.

They’re allowing active crypto traders to interact directly with the orderbook such that they can route to exchanges to see exact pricing.

Though not explicitly stated, we might even see them explore launching an Ethereum-based layer 2, following in Coinbase’s footsteps with Base.

CEX vs DEX dynamic

Historically, attention has gone to decentralized exchanges (DEXs) for two reasons: 1) centralized exchanges (CEXs) had insane KYC requirements, and 2) DEXs were the only way to trade long-tail assets. With Trump in office, KYC and compliance requirements will likely be loosened, and the regulatory friction to post more long-tail assets will be reduced. In this way, CEXs will be favorably positioned to capture even more market share, and continue to wrap defi primitives that decentralized venues would otherwise dominate. However, if CEXs continue to lag on the listing front, platforms like Hyperliquid — notorious for listing in hours, if not minutes — will become increasingly competitive. Hyperliquid bulls also argue that the BTC that users trade on CEXs is “wrapped” in the sense that users’ balance is just an entry in a database; deposits and withdrawals are onchain, but trades themselves are not (they’re just shuffling entries).

Embedded yield, globally

The trend of packaging and exporting defi is manifesting globally as well. Products in emerging markets — namely Latin America — are already exploring safe, passive yield (read: wrapped defi) for their customer base to tap into. Lemon Cash, a popular crypto platform in Argentina, launched a module where users can earn yield on their deposits via Aave — all directly within their app. Mountain Protocol, which is integrated into certain Latin American retail venues and exchanges, allows users to earn yield via their stablecoin, USDM. In January, Nubank (popular in Brazil) started offering 4% USDC yield to their customer base, and noted that the amount of USDC held by their customers increased tenfold last year. DolarApp currently offers a premium plan ($6.99/month) where users get 4% APY along with other benefits like 1% cashback in local spending and 1 free international transfer per month.

Automatically sharing yield with consumers will soon be the new status quo, and both fintechs and crypto companies who don’t offer products like these will fall behind. Obviously, not all yield is created equal and some platforms might offer higher, less safe yields in the attempt to grow their market share. As companies compete to offer the most attractive and safe yields, wrapping defi products will continue to popularize beyond just stablecoin yield — for better or for worse.

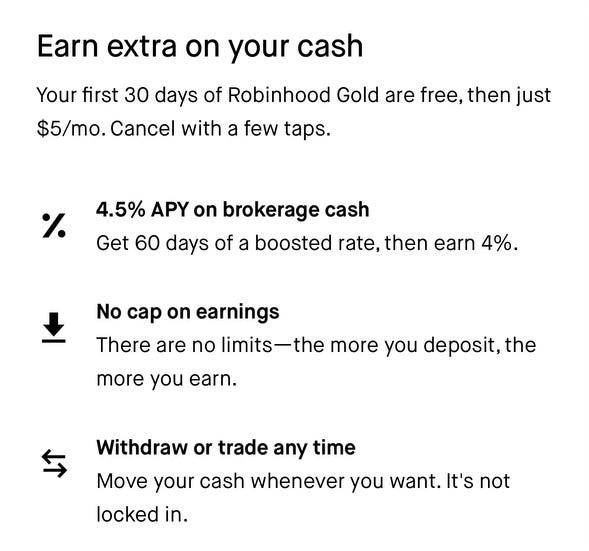

Latin America is a first mover here, but popular U.S.-based fintech platforms are also starting to offer yield, which consumers are increasingly recognizing as the new normal. Right now, Coinbase automatically offers 4.1% APY on any USDC held on their platform, and Robinhood offers 4.5% APY for Robinhood Gold subscribers on cash held in their account (priced at $5/month). In Q4, more than 30% of newly funded accounts on Robinhood ended the quarter as Gold subscribers, showing the success of the platform as a home for savings, not just trading. Additionally, Robinhood is working on USDG — a global stablecoin they’re launching with other leading fintechs — which they plan to leverage to pass yield back to consumers (cue Vlad: “we think this is the future”).

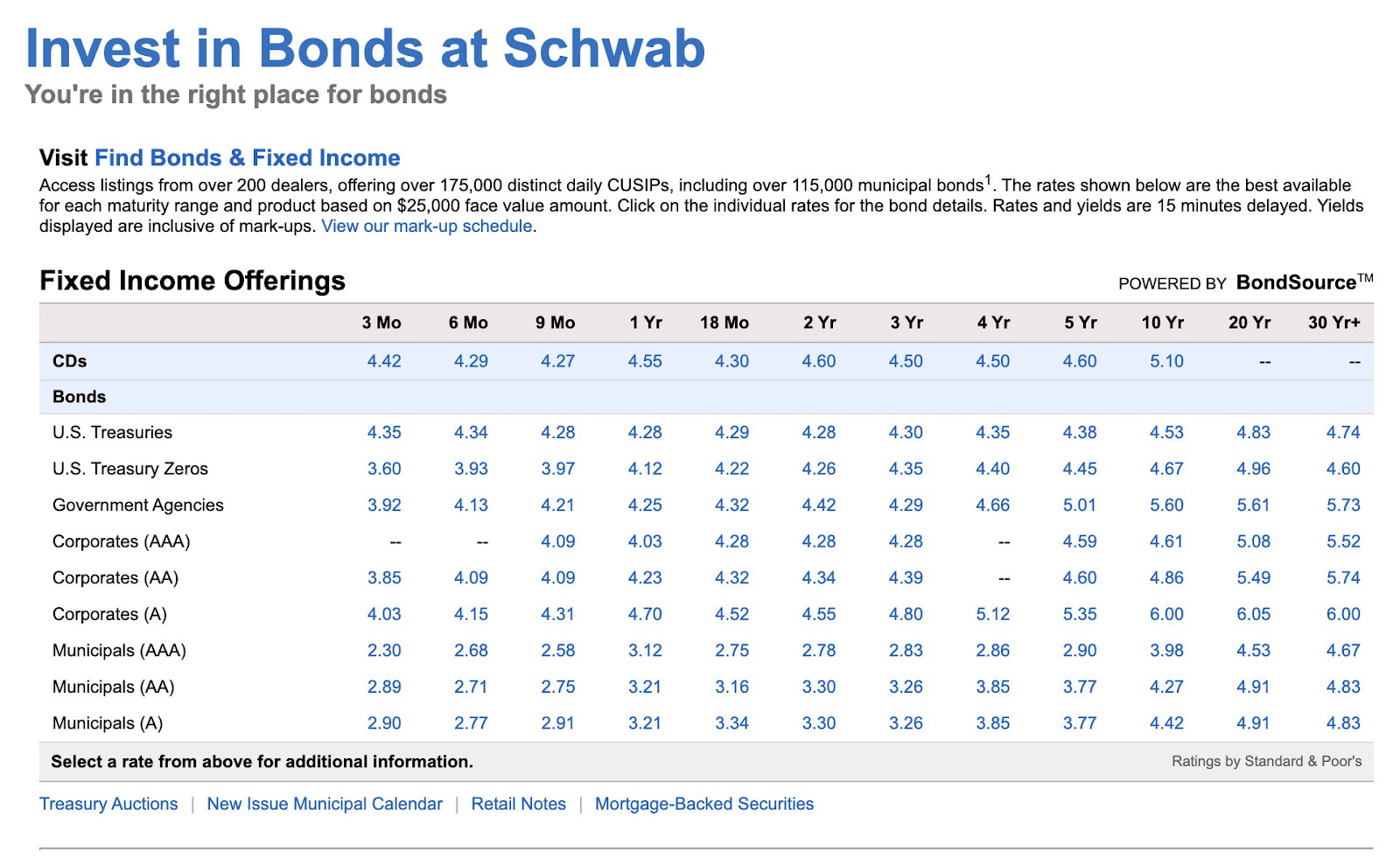

These platforms are also much more seamless than, say, Schwab, which looks like this when users try to earn ~4% on their balance:

Market dynamics & consumer behavior

One of crypto’s killer use cases with the best product market fit is just being able to earn passively. Ultimately, some users get discouraged and leave trading apps if they’re not making money on them — or, they simply run out of money to even spend on them. It’s a bit sad and ironic that in an era of Trump "winning," normal retail will lose more money than ever before via memecoins and probably altcoins too. On Pump.fun, for instance, 99.6% of users never realize more than $10,000 in profits — a large portion of this cohort actually loses money. When the $TRUMP memecoin launched, less than 1% of users who onboarded to crypto to buy it via Moonshot did anything else onchain. Presumably, this is because these users promptly lost money and became discouraged.

Of course, this experience isn’t unique to crypto (although it’s exacerbated in crypto because of the market’s volatile nature). For many retail participants, participating on stock trading platforms is a losing game under the guise of “financial freedom.” This promise of quick money — an insanely tempting one — then exploits and capitalizes on one of the most powerful human addictions: gambling.

One study found that increases in the number of Robinhood users are often accompanied by large price spikes followed by reliably negative returns — in other words, the market manifestation of hype-chasing. Further, “the layout of the [Robinhood] app, which draws attention to the most active stocks, also causes traders to buy stocks more aggressively than other retail investors.” Sophisticated short sellers then capitalize on these Robinhood trading patterns, and the cycle continues. Sadly, the outcome for these retail investors is rarely actual financial freedom, but rather addictive hopes of making life-changing money.

I believe that when the dust settles, attention — and capital — will gravitate towards products that passively allow users to make more money than they would otherwise have (be it within platforms like Robinhood on their different product lines like their savings offerings, or on new apps entirely). These true consumer surplus offerings — powered by crypto — are a way for users to protect and safely build their wealth rather than lighting it on fire.

If we as an industry are being honest, we are no longer onboarding net new people to defi with the current UX: it’s still too difficult for the average user. More generally, retail should be offered a better way: one where they at least have the option to earn via defi primitives without having to manually go onchain.

There are a number of newer projects tackling this today. Users can earn through direct-to-consumer products (mobile apps or web apps) or institutional-grade platforms:

Ondo’s USDY, which is tradeable on 8 chains including Solana, accrues yield daily (via T-bills) — whether the user is staking, borrowing, pledging, or just holding.

Tokenized yield products on Superstate, such as USTB (T-bills) and USCC (cash & carry — ~13.5% 30-day yield), leverage risk-free assets that can be represented onchain and cater to institutional customers, which can then pass on the yield to their end users.

Platforms like Stable, which wraps Aave into a clean UX, allow users to one-click deposit via ApplePay or their bank account, do a quick KYC via Plaid, and start earning immediately.

Leveraging existing networks is a great way to bootstrap a new form of money: Ethena, for example, is embedding their product directly within Telegram so users can access sUSDe functionality (earn, spend, and send) without leaving the app.

Kiln is using their existing B2B2C distribution to go after wallets, exchanges, and custodians to eventually power yield generation in the background depending on the end user’s risk appetite.

Products like Agro and Spark allows users to earn yield via stablecoins in a safe, passive way with minimal work required by the end user.

The ultimate distribution mechanism would be to just tokenize deposits of existing banks or neobanks such that customers get yield automatically — more on that in this stablecoin bank piece. Of course, it’s never in a traditional bank’s interest to automatically pass yield to consumers — or even to make it easy for them. But a status quo becomes a status quo over time, and there are always baby steps along the way.

Risks & lessons learned

What’s old is new again, and many people are trying to bring ideas from the past few cycles back because they’re now encouraged by incoming regulatory clarity as well as technical advancements that make previously infeasible ideas possible. As noted before, not all yield is created equal, and there’s always some level of smart contract risk that comes with cefi platforms wrapping defi. Problems around liquidation, rehypothecation, and system design — not to mention company-level debacles like Celsius trying to be a centralized version of Aave — are all worth considering. Hopefully, though, we’ve learned lessons from last cycle (I’d be remiss to not do a short section on risk in a post like this, but it seems like projects are proceeding with caution).

Closing thoughts

The next era of consumer finance is happening right now, and hopefully, it’s one that puts a bit more power (or cash / stablecoins) into the hands of the end user. Some may argue that cefi platforms wrapping defi defeats the whole purpose, while others think that it just exports defi to a broader audience via a better frontend — e.g., in the limit, cefi is just a frontend for defi. Maybe it was never cefi versus defi, but instead about bridging the two safely. Either way, it’s an interesting dynamic, and importantly, an opportunity for new winners to be created.

Thank you to Joey, Jon, Natalia, Dio, AP, George, & Addison, for discussion / review / thoughts that helped me on this.

Check out vaults.fyi

Our Earn API endpoints make it seamless to integrate DeFi experiences into your product by enabling a unified interface across dozens of staking and lending protocols. We already support dozens of protocols (AAVE, Compound, Morpho, Euler, etc.) and are working with early design partners on initial integrations.

Our own app (app.vaults.fyi) is a great way to see the functionality enabled by the APIs.

Great blog, and definitely a trend that is starting to arise. Be on the lookout for Votre.xyz doing the same thing...